Greenhouse gas emissions: Introduction to the reporting of greenhouse gas emissions to measure, record and reduce greenhouse gas emissions

Greenhouse gas emissions: compact introduction to reporting

In the efforts to decarbonize in order to reduce climate change, it is highly relevant to efficiently measure, record and reduce greenhouse gas emissions that occur.

The Greenhouse Gas Protocol (GHG Protocol) as a standard for the accounting of greenhouse gas emissions, GHG for short, provides a basis for the recording of GHGs in companies. Emissions are assigned to one of three emission categories, the so-called scopes. Based on this classification, a balance sheet is then drawn up. Organizations are often unaware of their GHG balance. The identification and categorization are the first steps to show which emissions are generated by the company’s activities. Based on this, optimization potentials can be identified, solution approaches can be developed and subsequently improvements can be achieved.

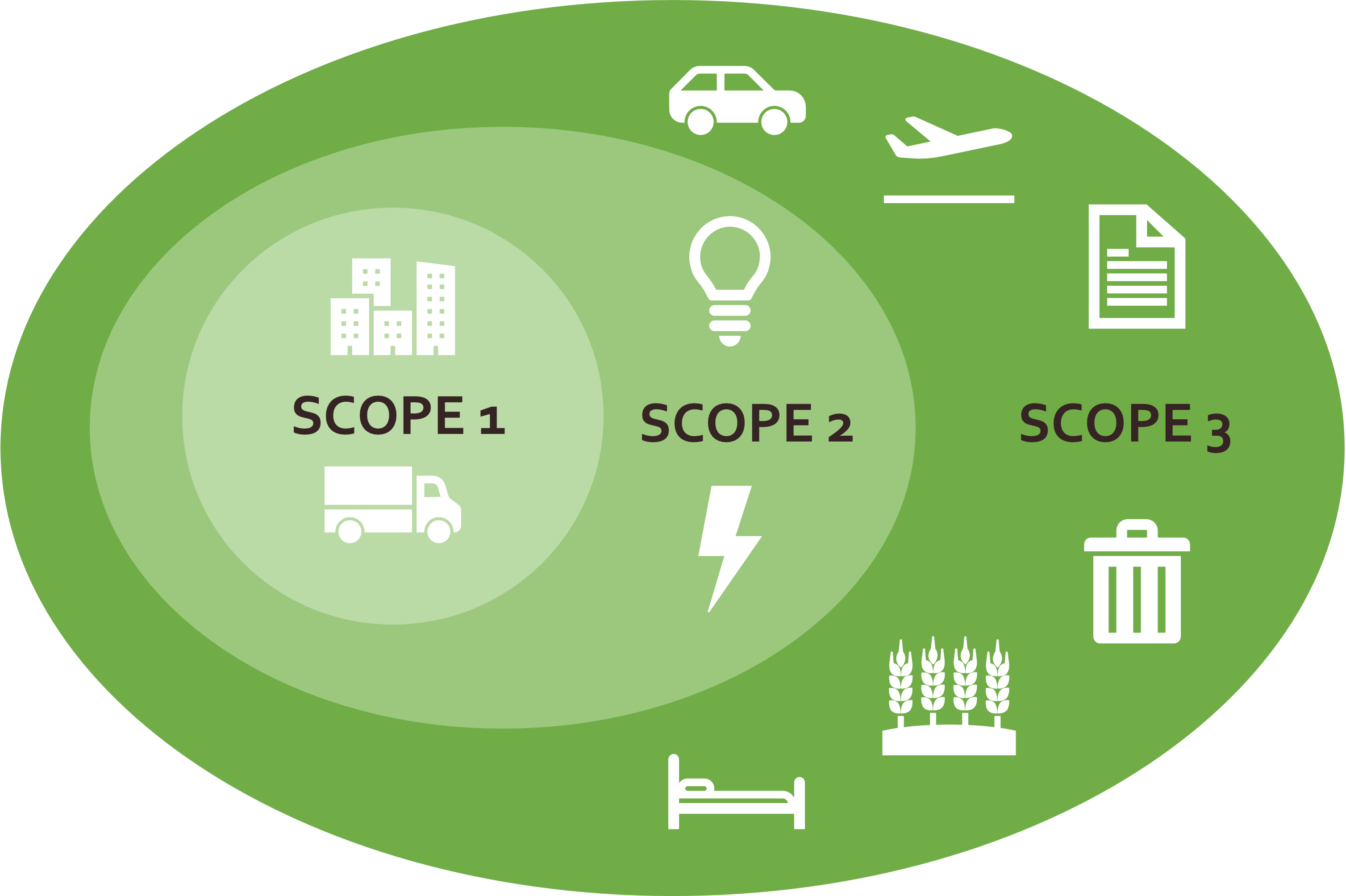

What are Scope 1,2 and 3 emissions?

Scope 1 – Emissions are direct emissions that occur in the organisation. These include the combustion of any fuel, the use of GHG-producing vehicles, and process-related emissions generated during industrial processes. This category also includes fugitive emissions, such as the release of refrigerant gases that can occur when air conditioning systems leak.

Scope 2 – Emissions are indirect emissions that result from the use of purchased energy for an organisation. This includes purchased electricity, steam as well as heat. In the case of own electricity production, the emissions that arise in the course of the process are accounted for as Scope 1 emissions.

Scope 3 – Emissions are further indirect emissions that do not fall into the Scope 2 category and occur in the company’s value chain. Scope 3 emissions can be divided into upstream and downstream emissions. Upstream emissions include greenhouse gas emissions associated with activities upstream of the company. These include, for example, the purchase of services and goods such as paper or transport routes to the company. Downstream emissions include indirect GHG emissions that occur when/after leaving the company. These include, for example, the sale and transport of produced goods and the disposal of waste. Other Scope 3 activities include the use of services and products, events, commuting and business travel.

Advantages for companies through Scopes Reporting

Recording and reporting emissions brings benefits for companies. The improved transparency can strengthen reputation and customer confidence. The aggregated presentation of all emissions contributes to a better understanding of risks related to resources and energy. Furthermore, hotspots and weak points in the entire value chain are identified. By identifying optimization potentials, energy and resource costs can be reduced if redesigned accordingly. Ultimately, compliance with the legal provisions on GHG reporting requirements or regarding CSRD is ensured with the help of the recording.

With the ESG Cockpit respectively the Impact Compass (Module for Common Good Balance Sheet), you can easily record your emissions digitally and document their progress.

(Lara Hammerl, Oktober 2022)